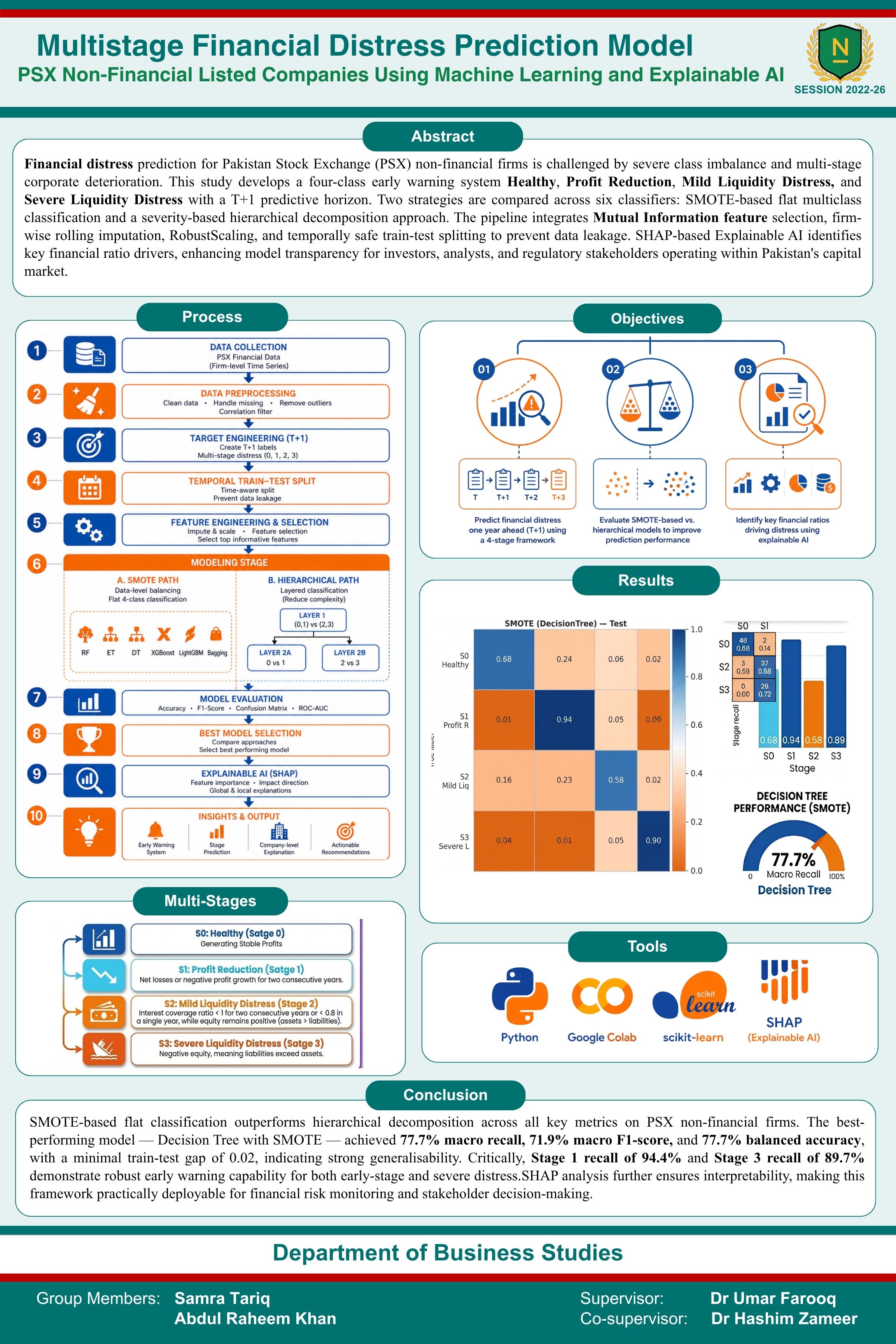

The financial distress models of the Pakistan Stock Exchange (PSX) companies are mostly binary framed, the class imbalance is not accounted for, time leakage is present in random splits, and the models are not explainable enough. It fills these gaps by developing a four-stage Early Warning System for 373 PSX non-financial firms (373 firms over the years 2011–2025) predicting distress in the subsequent year as being Healthy, Profit Reduction, Mild Liquidity Distress, or Severe Liquidity Distress in the target regime of T+1. This is done by using a rolling-mean imputation window=5, correlation filtering 0.98 and RobustScaling. Two imbalance strategies are compared using the same protocols; in-pipeline SMOTE and hierarchical decomposition ({0,1} vs {2,3}) with layer-specific features and exposure-bias correction. TimeSeriesSplit is used for the cross validation technique, and the six classifiers (Random Forest, Extra Trees, Decision Tree, LightGBM, XGBoost, Bagging) are tuned using RandomizedSearchCV, with the aim of maximising Macro Recall. SMOTE with Decision Tree wins: Macro Recall 0.777, Stage 1 Recall 0.944, Stage 3 Recall 0.897, Train–Test Gap −0.020. The current-year distress driver is the strongest Stage 3 driver (SHAP difference 0.918) and the bootstrap stability indicates reliability in the explanation (CV<0.10), with year-on-year persistence. The system provides meaningful and actionable risk alerts up to one year in advance before trouble arise.

Tools: Machine Learning,Explainable AI,Phython,Google Collab

Department: Department of Business Studies

Poster